Beyond the Construction Budget: A Justice Facility Leader’s Guide to Total Cost of Ownership

A few months ago, I was sitting across the table from a county official who kept repeating a version of the same request: “Just give me a number. One number. What’s this facility going to cost?” I’ve been in that room many times. And I always think of the same analogy when it happens.

Imagine a young couple asking a parent: “We want to start a family. How much does that cost?” The parent who answers with a single number isn’t being helpful, they’re being incomplete. Starting a family doesn’t cost a specific number. It sets off a cascade of financial events, some obvious and immediate, others slow-building and easy to overlook until they arrive all at once.

There are the direct costs you can plan for: the hospital bills, the crib, the diapers. And then there are the costs that compound over time and reshape a family’s entire financial picture: childcare, a bigger house and a bigger car, a possible adjustment to one income during parental leave, the orthodontist, the college tuition…etc.

No single number captures any of that. And no single number captures the true cost of building and operating a justice facility, either. That’s the essence of Total Cost of Ownership – and it’s the lens through which every criminal justice leader responsible for a facility should be thinking about their finances.

So, What Is Total Cost of Ownership?

A Total Cost of Ownership (TCO) model is a projection of all the costs an organization can expect to see over the life of a facility. Not just the construction budget. Not just the annual operating line. Everything: construction costs, debt repayment, staffing, inmate services, preventive maintenance, lifecycle replacement of building systems and equipment, utilities, transportation – every cost that is going to touch that organization’s bottom line because of that facility, for as long as that facility is in operation.

The model is built on one simple idea: if facility owners can see their costs, they have a greater opportunity to manage their finances. But if owners can’t see or understand their costs, that significantly limits their ability to manage those costs and their budgets effectively.

That sounds obvious when you say it out loud. But the reality is that most jurisdictions planning a new justice facility are focused almost entirely on the construction budget – which, while significant, represents only a portion of what an organization will actually spend over the life of that facility. The TCO model is designed to show the full picture. Not just the part that’s easiest to see.

You cannot look at a justice facility’s physical plant in isolation from the operations that occur inside it, any more than you can separate a family home from the life being lived within it. A TCO model is the mathematical expression of that principle – it puts all the costs associated with building and running a complete justice operation in one place, so that leaders can see them, understand them, and plan for them together.

The Baby Shower Only Covers the Crib

When a county approves a new jail, what gets discussed in that meeting is almost always the construction project budget. That makes sense – it’s the most visible cost and it’s what gets debated in budget hearings and reported in the local paper. But here’s what those conversations typically miss: in a complete 30-to-50-year TCO model, construction debt repayment typically represents around 40% of total costs, which is significant, but far from the whole story.

Then there are the costs that don’t always make it into the budget conversation at all: inmate services including medical care, food service, and programming; preventive maintenance; lifecycle replacement of building systems; utilities; transportation; liability insurance; workers’ compensation; legal reserves. Each of these is real. Each compounds over time. And none of them disappear because they weren’t budgeted for.

This is the family that keeps growing whether or not you planned for it. The baby shower covers the crib. It doesn’t cover the braces, the car insurance, or the college tuition – and those costs are coming regardless.

Note: These numbers are approximations and will vary according to the size, location and other specifications of the facility in question.

Why Everything Has to Be Seen Together

There is an inseparable link between a facility’s physical plant and the operations that occur within it. Everything must be considered together – rather than in the isolated silos that most budget processes create – because the decisions made in one area directly affect the costs in another. You cannot separate them.

Let’s consider a real-world example: HVAC systems. Central utility plants are typically more expensive to design and build than standard package units. In a purely construction-cost conversation, the package units win. But when you extend the analysis over the life of the equipment and factor in energy efficiency, maintenance costs, and system lifespan, central plants are typically the more cost-effective investment. The problem is that the person evaluating the construction bid and the person managing the facility’s operating budget are often different people, having different conversations, years apart. A TCO model puts them in the same room, looking at the same numbers, at the same time.

The same dynamic applies to facility layout and design. A facility with one central location for inmate services may be smaller and cheaper to build, but it may require significantly more staff to move inmates throughout the building over its lifetime. A facility with services dispersed across housing pods may cost more upfront but produce meaningful staffing efficiencies that save millions over a 30-year operating period. You only see that trade-off clearly when you’re looking at the total picture.

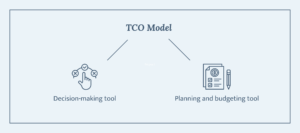

Two Tools in One: Decision-Making and Long-Term Budgeting

One of the things that surprises people when they first engage with a TCO model is that it serves two distinct but equally important functions: it is both a decision-making tool and a planning and budgeting tool. Understanding both is critical for any leader embarking on a major facility project.

Think of it like the financial planning a young family does over time. In the early years, the big decisions are still being made – where to live, whether one parent will stay home, what kind of car to buy. Those decisions are made with an eye toward long-term cost, not just immediate affordability. That’s the TCO model as a decision-making tool. In the early stages of a project, when major design, operational, and financing decisions have yet to be made, the TCO model helps leadership understand the projected cost impacts of each option in front of them. These early-stage models are built more on benchmarks, assumptions, and professional judgment, but they are still enormously valuable because they help people begin to see and digest the full financial picture before choices get locked in.

Later, as that same family settles into a routine and starts planning around actual income and actual expenses, the financial tool shifts in nature. It becomes less about deciding and more about budgeting and making sure the money is allocated for what’s coming. A TCO model evolves in exactly the same way. In the later stages of a project, and especially after a facility opens, the model transitions into a planning and budgeting tool. Actual costs replace assumptions. Real operational data refines projections. And administrators gain the ability to request and justify budgets with a level of precision that simply isn’t possible when looking at costs piecemeal.

The goal in both cases is the same: to have the funds available when they’re needed, rather than scrambling to find them after a problem has already arrived. A family that hasn’t saved for college by the time their child is seventeen isn’t facing a planning problem, they’re facing a crisis. Similarly, a facility that hasn’t funded lifecycle replacement of its mechanical systems isn’t facing a maintenance issue, it’s facing an emergency. Proactive planning, in both cases, is always preferable to reactive funding requests.

What Happens When the Money Isn’t There

We’ve all heard the saying, “money can’t buy happiness.” But don’t forget a related truth – a lack of money typically leads to unhappiness.

Having appropriate funding does not guarantee that an organization will achieve the outcomes it wants. But if an organization does not have appropriate funding levels, we know that one or more areas will be neglected – whether that be staffing, inmate services, or possibly facility maintenance or lifecycle replacement. Something always gives – and in a justice facility, the consequences of any one of those things giving way are severe.

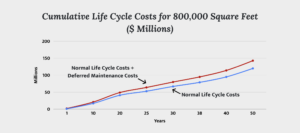

Criminal justice facilities are not schools or office buildings that go quiet after hours. These are 24/7 operations with intensive use that accelerates wear on every building system. When something breaks in a school, you close for a couple of days and make the repair. You cannot let a thousand incarcerated individuals out while you fix the HVAC. The stakes of deferred maintenance are simply higher, and the consequences of system failures are more immediate and more severe than in almost any other building type.

People can often see construction costs clearly, but they don’t always do a good job of setting aside money for preventive maintenance and lifecycle replacement. If we can show projected maintenance and lifecycle replacement costs to a client on the front end – and help them understand why they need to set aside that money, both for yearly upkeep and for long-term replacement of building components and equipment – then they have a long runway to program those costs into their budgets. When the time comes to replace a roof or critical mechanical equipment, the money is already there. It becomes a planned project rather than an emergency. And that distinction matters enormously, for operators, for facility managers, and for the elected officials who ultimately must come up with the funding or face the consequences of not doing so.

When to Start Considering TCO (Spoiler Alert: Earlier Than You Think)

One of the most common mistakes a jurisdiction can make is waiting too long to develop a TCO model. The instinct is understandable: “Why evaluate costs when so many decisions are still unmade? Wait until the program is finalized, the design is complete, the financing is structured, then we’ll do a cost analysis.”

But the value of a TCO model is greatest precisely when uncertainty is highest. Early-stage models give leadership the opportunity to begin absorbing the full scope of what they’re committing to, before decisions are locked in. Every major decision made without a TCO model in the room is a decision made without complete information.

It is never too early. In fact, we are producing some models now before a project has even formally kicked off. And those early models, even with their assumptions, fundamentally change the conversation because they show people the full family portrait, not just the baby announcement. Early iterations involve a lot of projections based on benchmarks, historical data, and professional judgment. Later iterations can incorporate actual facility size, actual staffing plans based on real floor plans, and real financing terms. The model gets sharper over time. But its value begins from the very first version.

Our recommendation is always to start the TCO process at the earliest opportunity, so people have the most time to see the cost picture, get comfortable with it, and plan around it.

The Most Important Thing to Understand About TCO (and the Most Common Mistake)

Cost is a very delicate topic. We often say that the first number someone hears will be the only number they remember. That means we must be careful about how we introduce TCO projections. It also means our clients need to clearly understand what a TCO model is, and what it isn’t.

A TCO model is a projection of costs based on our understanding of the situation as it exists at a given point in time. It is not a one-time document that delivers a definitive answer. It is a continuous tool that provides continuously updated projections. As future factors move from assumption to reality, the model adjusts accordingly. If an initial model assumes a certain rate of inflation and that rate changes, the model changes. If an outside authority imposes a new operational requirement on an organization, the costs change accordingly.

The most damaging misconception is treating a TCO projection as a promise. I sometimes explain it this way: imagine asking a warden to guarantee that an inmate who served their entire sentence, went through every rehabilitation program, and did everything asked of them would never break the law again. No honest warden would make that guarantee. What they might say is, “we set this person up for success. We gave them every tool available. But what happens after they walk out the door is beyond our control. Anyone who claims they can guarantee that outcome probably doesn’t understand what they’re talking about.”

In the same way, we can make very reasonable projections about future costs — grounded in our team’s collective experience, our data, and our professional judgment. But anyone who claims to project future costs with absolute certainty probably doesn’t understand the reality of what they’re doing. The value of a TCO model is not that it eliminates uncertainty. It’s that it gives clients the framework to see, plan for, and manage that uncertainty over time.

What Building a TCO Model Actually Looks Like

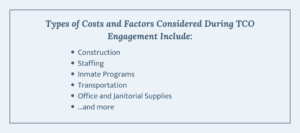

Contrary to popular assumption, a TCO model doesn’t start with a spreadsheet. It starts with a conversation – a deep, structured conversation with the client and the project team about every dimension of how the facility will be designed, financed, built, and operated. We work through approximately 75 different cost items and factors at the beginning of every TCO engagement. We gather existing cost data from current operations. We discuss every assumption that will go into the model and agree on them with the client before any numbers are run. It doesn’t do anyone any good to build a model based on assumptions that are still in dispute.

Take project financing as one example. How will the project be paid for? Through appropriations and cash on hand, through bond financing, or a combination of both? If bonds, what interest rate is realistic given the jurisdiction’s credit rating? What repayment period – we typically assume 30 years, but every situation is different. Would the debt be issued in one series or multiple? These details matter more than most people realize. We recently worked through a model where the assumed interest rate dropped from 5% to 3.5% between iterations. That single change (one and a half percentage points) translated to roughly $20 million less in annual debt repayment cost. A single assumption, properly refined, can reshape the entire picture.

Once we’ve agreed on all the assumptions and built the model, we schedule time to sit with the client and walk through it in person, line by line, year by year. We try to get as much time as they’ll give us — ideally an entire afternoon. And we present in as small a group as is practical, because you want an environment where people feel genuinely comfortable asking questions and making sure they understand everything being presented.

That in-person approach isn’t just a logistical preference. It reflects something important about how we think about our role. Our job is not simply to hand over a set of projections – it’s to educate our clients well enough that they can use that information effectively and accurately convey it to others who weren’t in the room. Decision makers are going to walk out of that meeting and explain these numbers to important stakeholders, such as commissioners, finance officers, and the public. They need to understand not just what the numbers say, but how we got there.

Who Needs to Be in the Room When Discussing TCO

When we engage in a TCO conversation, we try to bring in a cross-section of the people who will be affected by and responsible for the facility’s finances over time. That means people from the operations side – wardens, detention directors – the people who will actually be running the facility day to day. It means facility managers who understand the physical plant, and county finance staff who will typically grasp the financial framework most quickly. And ideally, it means at least one decision maker – a commissioner, a city councilperson – someone who will ultimately be the champion for the funding that the TCO model is designed to justify.

Sometimes it makes sense to present to different groups separately – finance people in one session, operational staff in another – because the questions and concerns those groups bring to the table are different. Regardless, the goal in every case is the same: a common understanding of the full cost picture, held by the right people, early enough to make a difference.

Remember the First Word: “Total”

I’ll close the way I always close this conversation, because it’s the thing I most want to stick:

If something is less than total, it’s incomplete. And it’s never a good idea to plan around incomplete data – particularly when the stakes are this high.

Want to lose sleep? We know two excellent methods: start a family or decide to build a justice facility. Neither will ever be easy. But as far as justice facilities are concerned, we believe that a thorough and continuously updated TCO Model will give you the peace of mind to rest easy, knowing that you have an accurate and realistic picture of the costs associated with your facility.

The family analogy works so well because it captures something true about how humans tend to process cost: we see what’s in front of us and underestimate what’s coming. A new facility feels like a building project, when in reality, it is a 30-to-50-year financial commitment that will touch every part of your organization’s budget, every year, for decades. Total Cost of Ownership doesn’t make that commitment smaller. It makes it visible. And when it’s visible, you can plan for it, budget for it, justify it, and ultimately fund it – proactively, rather than reactively.

The family you’re starting is going to need a college fund. The time to open that account is now.

Download the PDF

Meet the Author